US business cycles & implications for investors

Unfavorable cyclical conditions pose risks to the typically positive Q4 seasonality cycles

US vs. The World, Financial Stress, Inverted Yield Curve and Geopolitical Stress

In this article, I will focus on macroeconomic cycles. Before delving into an analysis of the performance of the US stock market or short-term cycles, it is essential to gain an understanding of these broader macroeconomic cycles that are at play.

Analyzing recent economic business cycles is crucial for investors and researchers in comprehending the present condition and future prospects of the US equity market. By examining these cycles, one can acquire insights into the patterns and trends that influence market behavior, enabling more knowledgeable investment choices.

In my previous presentations earlier this year, I discussed the significant long-term cycles and provided updates and forecasts for this year. These cycle patterns are now approaching critical periods, prompting a need to review and revisit these cycle models.

Bottom line

The adverse effects of extended periods of downturns in the long-term business cycles, as discussed in this article, can potentially jeopardize the traditionally advantageous year-end seasonality observed during the fourth quarter.

Now, lets get into the cycle models.

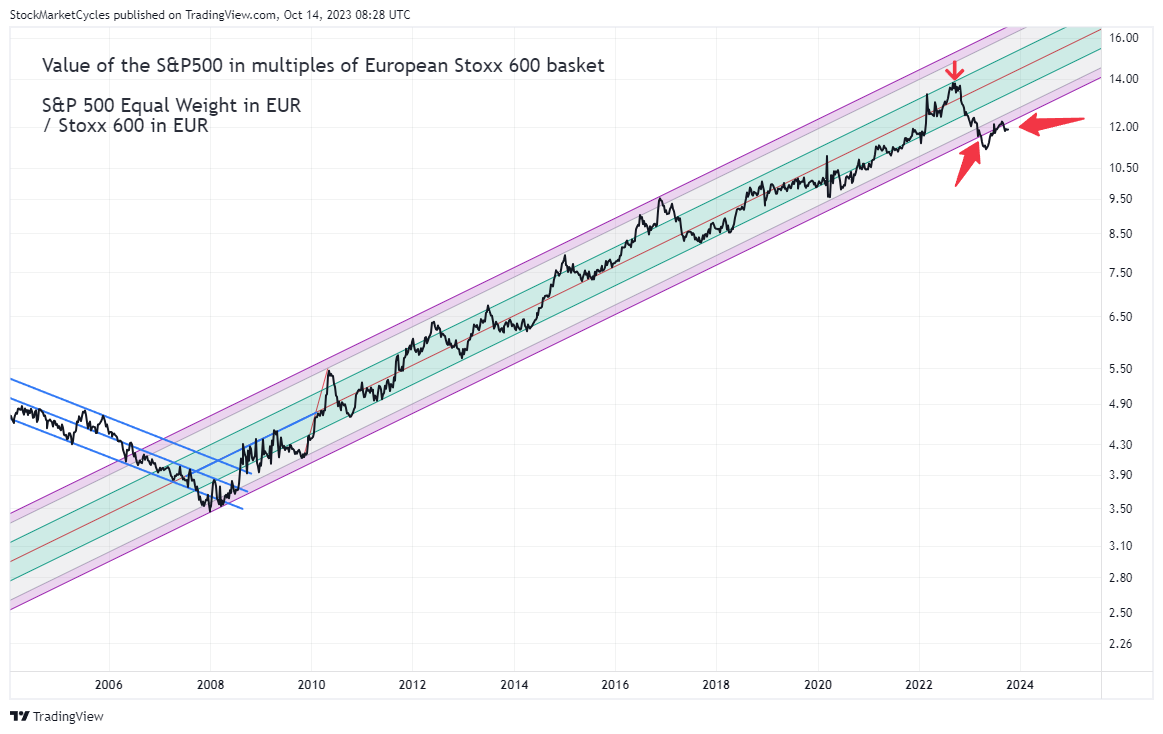

(1) The end of linear outperformance | US vs. The World

Lets start with a long term trend change of the US business cycle in comparison to other countries.

In analyzing the long-term trend change of the US business cycle in relation to other countries, a noteworthy cyclic phase of growth spanning 15 years appears to have reached its culmination in 2022. This observation suggests that compared to the global investment markets, the performance potential of the US market may be comparatively subdued.

The shift in trend within the US business cycle holds significant ramifications for equity markets. Recent research studies by Avramov and Chordia highlight an important connection between predictability of cross-sectional equity returns and consideration of variables relating to different stages within a business cycle. These findings indicate that inefficiencies present in financial markets can be attributed to participants failing to incorporate into their analysis The changing structural dynamics inherent within economic regimes.

In ”The illusion of a healthy U.S. stock market”, I first shared this chart.

The updated chart below reflects the recent data, showing that there was a breakout to the downside of the channel in early 2023. The first time for 15 years. Despite attempts to recover and reenter the upsloping trend channel during the course of the year, this has not been successful thus far.

From an international viewpoint, it appears that the long-standing outperformance of US equities has ceased. There are currently no indications suggesting a reversal back into a positive channel.

The implications of the chart above and the breakout to the downside are vast. The traditional linear thinking that has governed the US economy and financial system is no longer applicable. For years, the US investment system relied on a linear global upward moving economy, with "riding that trend" by printing more money as its guiding principle. However, considering the chart displayed earlier, it is doubtful whether this linear thinking will be successful in navigating through the forthcoming cyclical downward phase.

Contrary to what was previously believed, relying solely on linear thinking may prove to be ineffective going forward. While stability calls for and benefits from such rational thought processes, today's world is characterized by dynamic tension where linearity falls short. As indicated by the chart presented here, it becomes evident that a paradigm shift away from conventional linear outperformance of the US economy is imperative for investment success in these volatile times.

The state of affairs depicted in this chart forces us to acknowledge that linear thinking alone can no longer sustain economic growth in the United States. It signifies a local decline cycle phase within US equity markets compared to other global economies and serves as an unmistakable call for embracing new modes of orientation.

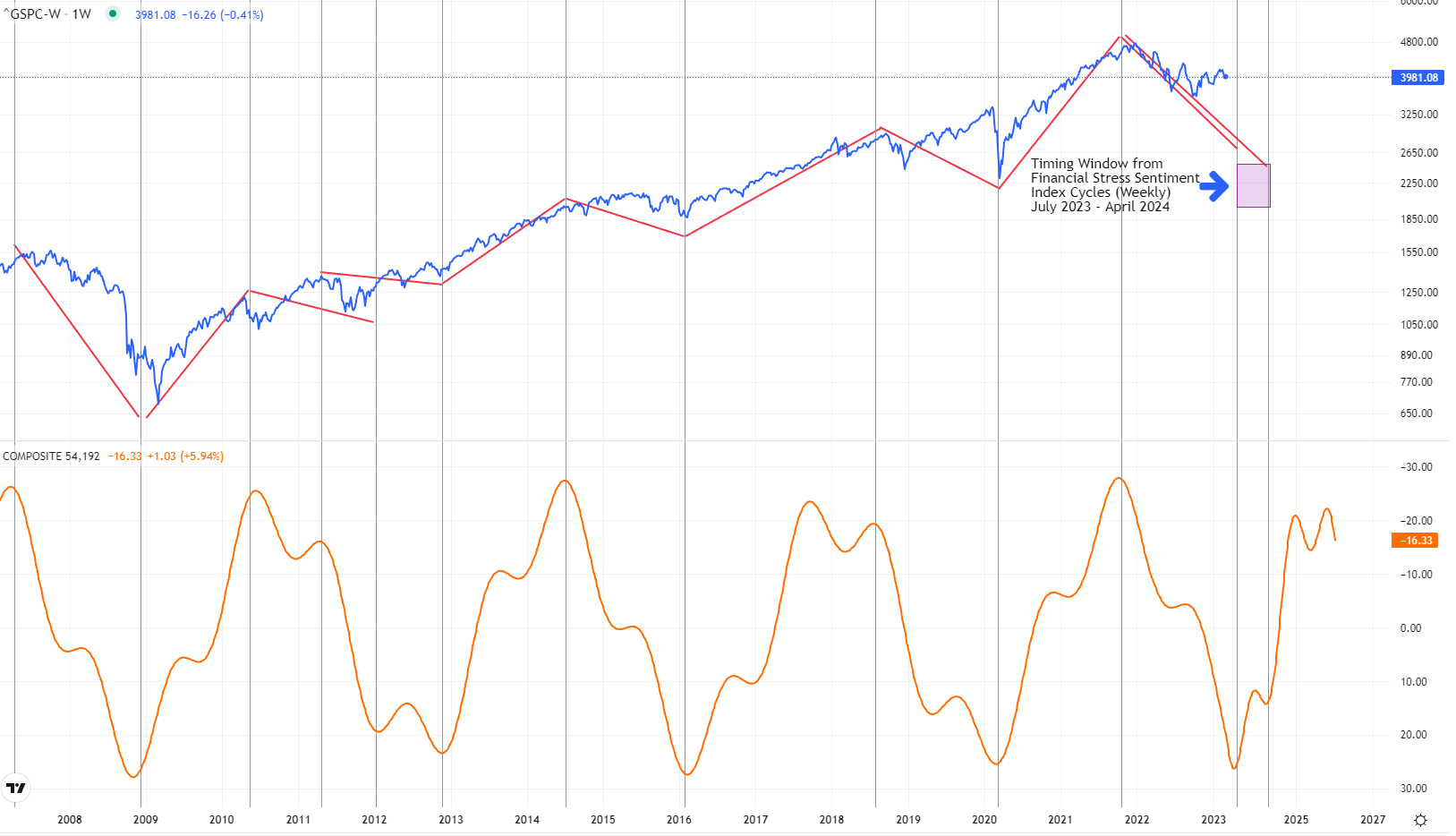

(2) Hot Financial Stress window is ON until April 2024

In the realm of finance, there exists a crucial and consequential aspect known as the financial stress window. This concept refers to a specific period of time during which the level of financial stress in an economy or financial market is particularly high and has significant implications for economic behavior and outcomes. Financial stress can be defined as a state of heightened pressure and strain in the financial system, often characterized by factors such as market volatility, increased uncertainty, deteriorating credit conditions, and a decline in financial institutions' ability to fulfill their intermediation role effectively. During a financial stress window, these indicators are intensified and can have far-reaching consequences for the overall functioning of the economy. These topping windows in Financial Stress often correlate with equity market bottoms.

One important and well-documented example of a financial stress window is the period from 2008 to 2009, commonly referred to as the global financial crisis. During this time, financial stress reached extreme levels as a result of the collapse of major financial institutions, a sharp contraction in credit availability, and plummeting stock markets.

This period of high financial stress had profound implications for the global economy, leading to a severe recession and widespread economic hardship. Numerous studies have demonstrated the detrimental impact of financial stress on economic activity(Romih et al., 2021). For instance, Hakkio and Keeton found that financial stress negatively affects economic activity in the US. They discovered that during periods of financial stress, there is a significant decrease in economic activity, leading to lower GDP growth rates and higher unemployment rates.

By analyzing the Financial Stress Index dataset provided by the Federal Reserve of St. Louis, we can identify and project significant cycles of financial stress. These cycles are characterized by periods of relative stability and low stress, followed by sharp increases in stress levels. We analyzed the Financial Stress Index data from the Federal Reserve of St. Louis to detect and project these important stress cycles into the future.

I shared the important underlying financial stress cycles and their respective topping and bottoming windows back in March this year in the section "Financial Stress Composite Sentiment Cycle". The financial stress composite cycle is shown inverted as indicator on the bottom of the next chart.

The hot and important cyclic window in financial stress refers to a specific period of time when the level of financial stress in an economy or financial market is particularly high and has significant implications for economic behavior and outcomes. It is now on and active!

This cyclic window typically includes periods of heightened market volatility, increased uncertainty, deteriorating credit conditions, and a decline in the ability of financial institutions to fulfill their role effectively. The detection and prediction of potential financial stress during these hot and important cyclic windows are of crucial importance (Christensen & Li, 2014).

We are now currently experiencing another significant period of financial stress due to the composite cycle, as indicated. This time frame, from July 2023 to April 2024, is particularly critical.

During this period of projected upcoming financial stress, it is essential for financial analysts to diligently observe and assess different indicators that reflect the level of strain within the US equity markets.

(3) Active recession alert due to yield curve inversion cycles model

Yield Curve inversion could indicate another upcoming recession for the US. The yield curve inversion has historically been a reliable indicator of an impending recession in the United States. Many studies and research have shown a strong relationship between yield curve inversions and the occurrence of recessions(Georgoutsos & Migiakis, 2013). Furthermore, the yield curve inversion has been a topic of numerous studies as it serves as a signal of investors' expectations.

To explore the patterns in the yield curve inversion, a careful analysis was conducted on the difference between 10-year and 1-year US treasury yields. The dataset revealed significant cycles within this relationship. It is noteworthy that major troughs in this curve have historically coincided with recessions, leading to declines of about 50% in US equities thereafter. Interestingly, it seems that we are approaching the end of this inversion phase, which typically precedes an impending recession.

Here is the model & reference:

Another study by Stock and Watson showed that in the United States, five out of the six recent inversions of the Treasury bond yield spread were followed shortly by business cycle peaks, indicating an upcoming recession(Alles, 1995).

This empirical evidence suggests that there is a strong relationship between yield curve inversion and future economic activity, specifically recessions.

At its current state, the previously inverted yield curve appears to be showing signs of returning to a more normal shape.

The phenomenon of an inverted yield curve, especially when it begins to transition back to a normal shape, has long been regarded as a significant indicator of the economy's future trajectory. Its effects on the overall economic performance may not become apparent until after the process of returning to its original form is underway.

This can be seen by the grey shared areas in the chart above which indicate US recessions after the yield curve reversed from the inverted to the normal state.

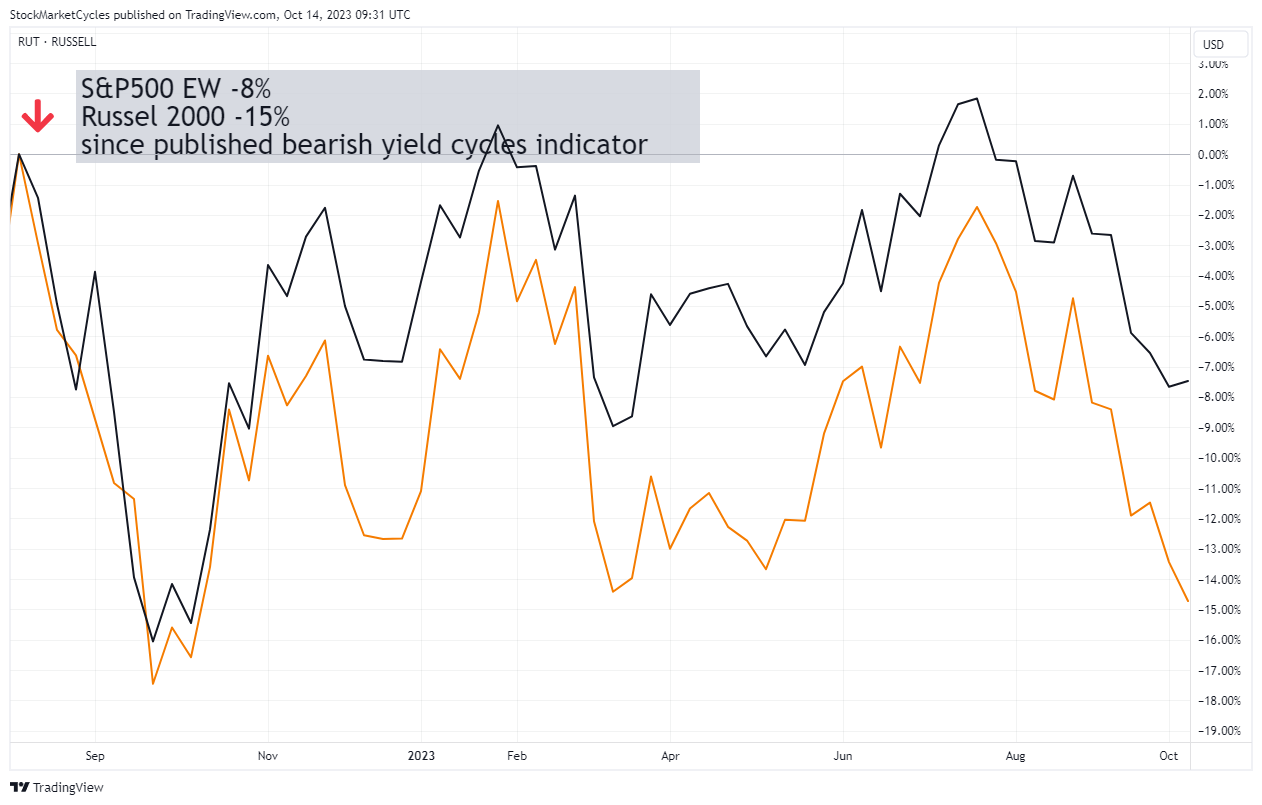

Our cycle model predicted that back in late 2021. Now the inversion of the yield curve that occurred in 2021 could be indicative of another upcoming recession for the US. The yield curve inversion model is leading the equity market by 6-12 month. So this window is still hot and on with more room to the downside.

Here is the performance so far since the release of this cyclic signal shown on the S&P 500 Equal Weight and the Russel 2000.

So we did the first -10% now, and these is still more room to the downside as the cyclic model suggests a possible potential of -50% for these kind of cyclic situations.

(4) Geopolitical cycles | by Forecaster David Murrin

During the Cycles Summit 2022 at the Foundation for The Study of Cycles, David Murrin, a geopolitical and financial market forecaster, presented his cyclic model. In this thought-provoking session titled "US Equities in the Decline of Empire," Murrin emphasized why he considers it to be a timely theme. I highly recommend taking a closer look at this segment from timestamp minute 50 to 1h 05min.

You will find the part of his presentation here in the public presentation.

You will find more about his work on his website at https://www.davidmurrin.co.uk/ .

Murrin's models are based on his own comprehensive analysis; however, it is intriguing how they align with our cycle models mentioned in this post.

(5) Lower highs and lower lows - a downtrend at work

In light of the macroeconomic cycles discussed, it is evident that the US equity markets are experiencing a downward trend characterized by declining lows and highs. Seen below in the mid- and small cap Russel 2000 and Microcap indices.

This serves as confirmation of the ongoing downtrend in this economic environment. We are still in the longer downward cycle leg of the overall composite cycles model.

Sure, and we all know that it is evident that the recent upward movement of the "Magnificent 7" stocks has significantly influenced and driven up the major indices in the US equity market. However, if we were to exclude these 7 stocks from our analysis, it becomes apparent that overall performance of the market in 2023 has been negative across all indices.

It becomes essential to remain vigilant during these significant periods of economic cyclicality highlighted in this article. At present, there is still a lack of key indicators suggesting that we have surpassed the bottom point outlined for these important economic cycles. Therefore, it appears that we have yet to reach the bottom phase.

So, finally, my quick wrap up:

These considerations suggest that the US stock market may encounter notable difficulties in achieving favorable year-end seasonality amid the current downward trajectory and uncertain conditions of the business cycle that have not yet reached critical bottoming periods.

In my upcoming next article, I will move to stock market as itself to analyze asset classes and their respective current cycle conditions. As the alignment of economic and financial cycles, as well as the movements in stock market prices, can provide insights into potential shifts in trends. That’s what we call “Synchrony of Cycles”.

Until then, I would be happy to hear your comments and ideas. I will take these into account in my deep-dive analysis during the next days. Please subscribe, if you have not already, to not miss the next issue.

As always, I have recorded a pod-cast audio commentary for my supporting paying subscribers. Please scroll at the bottom of the article past the disclaimer to get to the audio commentary.

Regards,

Lars

© 2023 lars.cycles.org, Lars von Thienen, All Rights Reserved.

Any reproduction, copying, or distribution, in whole or in part, is prohibited without permission from the publisher.

Information contained on this site is obtained from sources believed to be reliable, but its accuracy cannot be guaranteed. Lars von Thienen “lars.cycles.org” is a publisher of scientific cycle analysis results for global markets and is not an investment advisor. The published analysis is not designed to meet your personal circumstances – we are not financial advisors and do not give personalized financial advice. The opinions and statements contained herein are the sole opinion of the author and are subject to change without notice. It may become outdated and there is no obligation to update any such information.

Any projections, market outlooks or estimates herein are forward looking statements and are inherently unreliable. They are based upon certain assumptions and should not be construed to be indicative of the events that will occur.

Investments should be made only after consulting with your financial advisor and only after reviewing the prospectus or financial statements of the company or companies in question. You shouldn’t make any decision based solely on what you read here.

Neither the publisher, the author nor any of its affiliates accepts any liability whatsoever for any direct or consequential loss howsoever arising, directly or indirectly, from any use of the information contained herein.